Why You Should Understand Medicare Surcharges

Nov 28, 2023 By Susan Kelly

The best way to protect yourself financially in a fire, natural disaster, or burglary is to get adequate homeowners and contents insurance. This is the case regardless of whether the occurrence is natural or artificial. To accomplish this, you can buy homeowner's insurance and a separate contents policy from the same carrier or compare prices and coverage amongst many insurers. A discount may be available if you purchase multiple plans from the same supplier simultaneously.

What You Should Understand About Medicare Surcharges

Surcharges For Medicare

During your time in the workforce, you made Medicare contributions. The federal government collected around 15 percent of your salary to pay for Medicare and Social Security. 3 When you retire, you may feel more at peace with all those years of deductions because you'll finally have access to comprehensive health coverage at a fraction of the cost you likely spent while working. You probably won't be able to meet all your medical expenses with just Original Medicare. It's common for seniors to buy Medicare Supplement insurance to fill in the gaps in their primary Medicare coverage. As a result, healthcare expenditures will continue to rise each month. In 2022, the average person will pay $170.10 for Medicare Part B, an increase of $21.60 from 2021's $148.50. You've been paying into Medicare for decades.

How To Calculate Medicare Surcharges

The Social Security Administration (SSA) uses your MAGI from the two years prior as the determining factor. This means that your current period's benefits will be determined by how much money you made two years ago. For the vast majority of taxpayers, MAGI and AGI will be identical. Still, your MAGI may differ if you make payments such as student loan interest, alimony, or moving fees. To establish whether or not you owe surcharges in 2022, the SSA will review your tax return from 2020. 5 This method is used since the Social Security Administration had only access to tax returns from the previous year when the levels are generally set.

How Much You Have To Pay

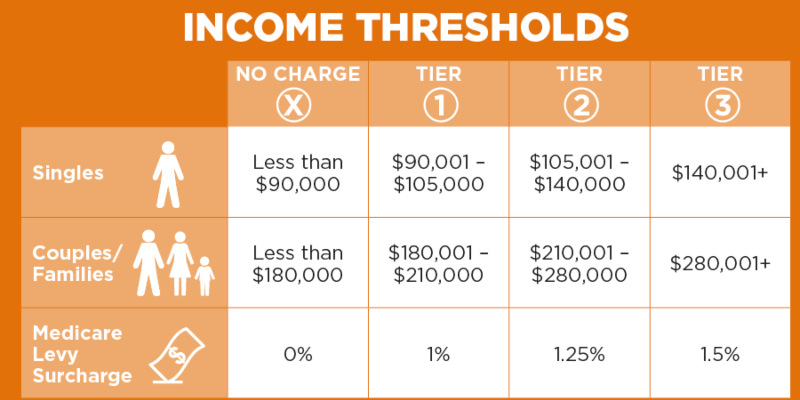

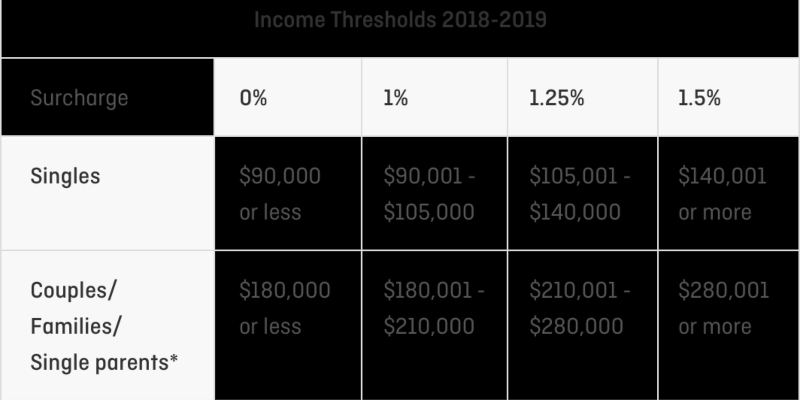

Although it's always preferable to avoid incurring extra costs wherever possible, there is some good news buried within those fees. First, as of the year 2022, the following is the breakdown of fees for those with MAGIs from the previous two years:

- For couples with a joint income of $182,000 to $228,000 or an individual income of $91,000 to $114,000, the Medicare Part B premium is $68 per month, and the Medicare Part D premium is $12.40 per month, respectively.

- If both spouses earned between $228,000 and $284,000 per year, the couple would pay an additional $170.10 per month for Part B and an additional $32.10 per month for Part D. If either spouse earned between $114,000 and $142,000 per year, the person would pay another $2.

- If both spouses worked and earned between $284,000 and $340,000 (or $142,000 and $170,000, respectively), the couple will pay an additional $272.20 per month for Part B and an additional $51.70 per month for Part D.

- A married couple makes between $340,001 and $750,000 per year, or if a single person makes between $170,000 and $500,000 per year, they must pay an additional $374.20 per month for Medicare Part B and $71.30 per month for Medicare Part D.

- If a married couple makes more than $750,000 per year together, or an individual makes more than $500,000 per year, the spouse who earns more will be responsible for paying an additional $408.20 per month for Part B and $77.90 per month for Part D.

Conclusion

Planning for Medicare and medical costs is crucial to any person's financial strategy. It's not uncommon for people to underestimate their out-of-pocket medical expenses and neglect to do anything about rising Medicare premiums. Thus, this article addresses Medicare planning concerns that CPA financial planners should address while guiding their customers. We'll cover the topics of Medicare tax basics, premium surcharge calculations, health care cost forecasts, and methods for easing the burden of rising Medicare expenditures for affluent patients. Since it was first introduced in 1966, Medicare has maintained its widespread support. In the United States, it covers the cost of medical care for those 65 and older and many younger persons with impairments or certain illnesses. For the vast majority of Medicare's existence, premiums were the same for everyone.